Reliable, data-driven intelligence is crucial for European companies seeking to compete effectively in the U.S. optical market. The newly released 2025 Market inSights with 2026 Forecast Report from The Vision Council sheds light on key developments across eye exams, eyewear, and retail performance. One of its central findings stands out: while the market continues to grow in value, consumers are purchasing fewer products overall. This shift raises important questions for manufacturers, suppliers, and retailers alike.

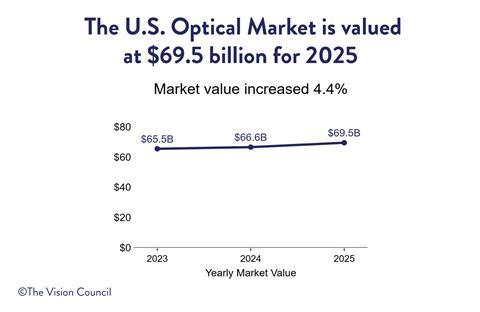

For more than two decades, the non-profit trade association The Vision Council has tracked the performance of the U.S. optical sector, which, with a total value of $69.5 billion, is one of the most attractive optical markets in the world. Its annual Market inSights Report measures the market’s actual performance using real-world data.

The analysis draws on millions of verified transactions, including patient billing records from thousands of practices, credit and debit card spending at more than 85,000 retail locations, and insights from a large-scale consumer survey of 48,000 respondents. The result is one of the most comprehensive and evidence-based assessments of the optical retail landscape available today.

The report covers all major segments of the market, including eye exams, eyeglass frames, lenses, contact lenses, plano sunglasses, and reading glasses. It also evaluates vision correction usage, participation in managed vision care programs, and the national footprint of optical retail.

These are the key findings from the ”2025 Market inSights Report”:

- Industry Value Growth Amid Volume Declines – The total market value increased modestly from 2024, reaching $69.5 billion. Ophthalmic lenses remained the highest-value prescription category, while plano sunglasses led non-prescription sales.

- Fewer Eye Exams, Higher Costs – The market value of eye exams continued to grow, despite fewer exams being conducted. The average cost of an exam increased by $10 compared to 2024.

- Shifting Consumer Behavior – Economic uncertainty and evolving tariff policy weighed on consumer sentiment, yet spending remained more resilient than typically expected during sentiment downturns. This suggests that consumers were selective rather than disengaged.

- Plano Sunglasses Recorded Volume Gains – Plano sunglasses saw a 2% increase in unit volume in 2025, even as volume declined across most other optical categories.

- Retail and Channel Dynamics – In-person purchases continued to dominate, with more than 80% of frames and lenses purchased in physical locations. Of all products, contact lenses had the highest percentage purchased online.

Alysse Henkel, The Vision Council’s Vice President of Research & inSights, explains what these findings mean in practice.

Compared to previous years, where do you see the most significant changes in the data?

Alysse Henkel: Three shifts stand out for companies watching the U.S. market. The first shift relates to the exam market. Exam value increased for the second consecutive year, but exam volume dropped to the lowest volume since 2022. The combination of rising prices and falling traffic suggests that consumers without strong insurance coverage are delaying care, which creates downstream pressure on product sales.

Second is the divergence between value and volume in prescription eyewear. Frames value also increased while volume declined. Lenses’ value slightly declined while volume fell. In prior years, these categories moved more closely together. The 2025 data reflects both pricing dynamics and a shift in consumer purchase behavior.

The last shift is seen regarding the stability of e-commerce. Despite expectations of continued online growth, the online share of frames and lenses has held steady for several years. U.S. consumers are not abandoning optical retail; they are choosing in-person experiences deliberately at a reasonably consistent pace.

What surprised you most about consumer behavior in the 2025 findings?

The resilience of consumer spending despite historically weak sentiment certainly stood out. Confidence measures were low throughout 2025, and tariff headlines created real uncertainty about price increases. Yet total market value grew $2.9 billion year-over-year.

What made this particularly notable is that volume declined across most categories at the same time. Consumers weren’t buying more frequently; they were spending more per transaction. That’s an unusual pattern. Typically, when sentiment falls, both volume and value soften together. In 2025, U.S. consumers were more selective about when to buy, but when they did buy, they didn’t trade down.

The market grew in value despite declining unit volume. What implications does this have for companies?

For companies evaluating the U.S. market, this dynamic has strategic implications. Growth driven by price increases rather than volume expansion can be sustainable if customers continue to see value in the premium product qualities – whether it be certain brand names, materials, durability or fit that they prioritize. But if price increases outpace perceived value, consumers may eventually pull back. We’re watching the price-volume relationship closely as we move further into 2026.

With more than 80% of frames and lenses still purchased in physical stores, what does this indicate about the ongoing role of brick-and-mortar retail in an increasingly digital marketplace?

Optical is structurally different from general retail. Eyeglasses require professional fitting, accurate measurements, and typically an in-person exam. Even contact lenses sales, which have the highest online penetration among prescription products, are still mostly purchased in-person.

Our data shows that consumers spend substantially more when they buy in-store for both frames and lenses. U.S. consumers value the expertise, service, and experience of optical retail, and they pay a premium for it.

For companies developing U.S. distribution strategies, this means that physical retail partnerships remain essential. Digital presence matters for brand discovery and consumer research, but the transaction still happens in the store for the vast majority of prescription eyewear.

What do these findings imply for inventory planning and assortment strategies as the industry looks toward 2026?

With unit volume under pressure and consumers being more selective, inventory efficiency is increasingly important. Carrying deep stock in slow-moving styles is riskier when store traffic is down and purchase cycles may be extending.

On assortment, a barbell strategy has merit: clear value at accessible price points alongside curated premium options. Plano sunglasses demonstrated this pattern in 2025, with strong performance at both ends of the price spectrum. Prescription eyewear may follow a similar logic, with opportunity in both opening price points and premium segments.

Still, tariff uncertainty adds complexity. Supply chain volatility favors lean inventory in theory, but execution is challenging when lead times are unpredictable. Companies operating in the U.S. market should stay close to real-time sell-through data and be prepared to adjust quickly rather than relying on historical seasonal patterns.

Where do you see the strongest growth opportunities for the optical industry/retail in 2026?

Contact lenses are positioned for recovery. After a volume decline in 2025, we forecast a volume increase in 2026. The category benefits from strong underlying drivers, including myopia management, daily disposables, and specialty lenses. Once consumers are fitted into contact lenses, they tend to repurchase regularly.

Premium ophthalmic lenses also represent an opportunity. Even with flat volume, we forecast a slight value increase as consumers continue to pay for features like photochromic treatments, blue light filtering, and progressive designs. Companies that can effectively communicate the benefits of lens upgrades are well-positioned.

One U.S.-specific factor to watch: tax refund season. Projections suggest refunds may be larger in 2026 due to recent tax law changes, and the optical industry has historically seen a spending bump when consumers receive windfall income. This is not a structural growth driver, but it could support a stronger first half.

The Vision Council operates at the intersection of market intelligence, strategy, and industry leadership. For companies and investors evaluating opportunities in the $69.5 billion U.S. optical market, access to objective, transaction-backed data is a competitive advantage. The organization produces a variety of recurring research publications, including the annual Market inSights report, quarterly Consumer inSights studies, semi-annual Provider inSights, and special interest Focused inSights reports.

Beyond syndicated research, The Vision Council designs fully customized research engagements tailored to specific strategic questions. Leveraging proprietary data assets, including anonymized patient transactions, credit card spending data, consumer and provider survey panels, and nationwide U.S. optical location intelligence, the inSights Research team designs and executes bespoke projects ranging from targeted surveys and focus groups to advanced market modeling and location analytics. All custom projects are exclusive and confidential, providing clients with proprietary insight to inform investment decisions, market entry strategy, product development, pricing architecture, and distribution planning.

For organizations with ongoing exposure to the U.S. optical market, membership in The Vision Council offers an additional strategic layer. Members receive complimentary access to flagship research reports, as well as preferred pricing on supplemental data products and custom research initiatives. Membership also provides direct engagement with industry leadership, advocacy representation, and early visibility into regulatory, trade, and market developments that shape operating conditions in the United States.

In a market where pricing dynamics, consumer selectivity, and supply chain uncertainty are reshaping performance metrics, disciplined growth depends on reliable, forward-looking intelligence.

For businesses and investors seeking clarity in the U.S. optical sector, The Vision Council provides data with decision-grade insight.

Explore subscription options, inquire about membership, or request a custom research consultation to gain a sharper view of where the market is heading next.